Key Takeaways:

- Your RSU cost basis is the fair market value of your shares on the vesting date. It sets the foundation for future capital gains tax.

- Selling shares immediately after vesting typically results in no capital gain, making RSUs a valuable tool for building liquidity.

- Capital gains taxes (either short-term or long-term) apply only on appreciation after the vesting date.

- Many high earners under withhold taxes at vesting, creating surprise liabilities later.

- Misreporting RSU cost basis is a common mistake that can artificially inflate your taxable income.

RSU Cost Basis, Taxation, and Reporting Summary: What Equity Holders Need to Know

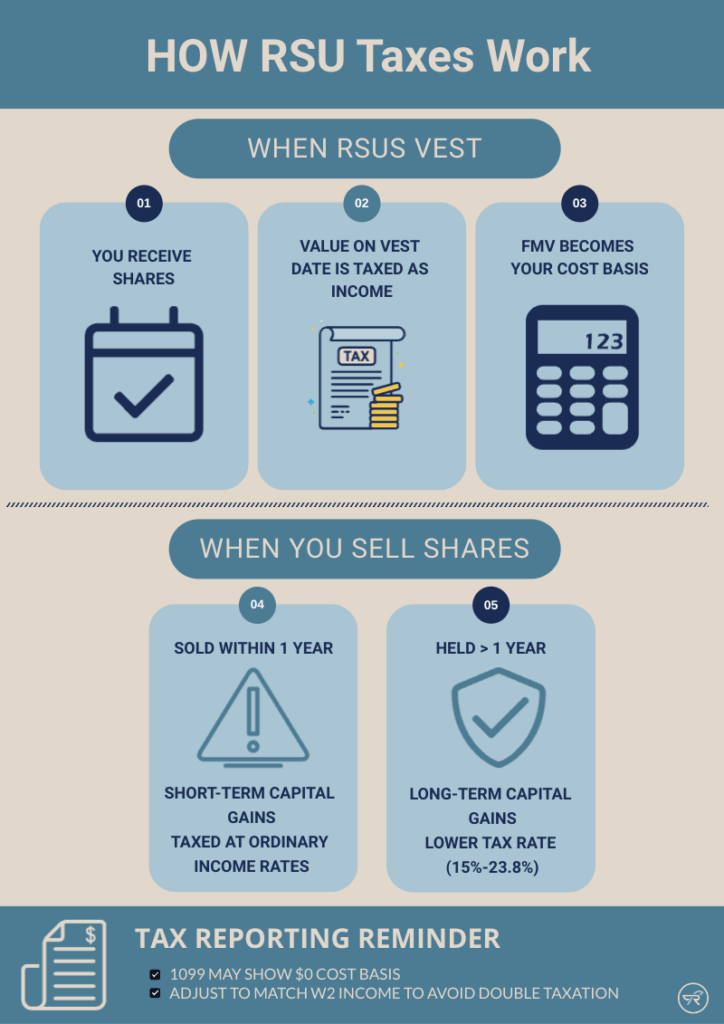

What is the Cost Basis of RSUs?

Your cost basis is the starting point for measuring gain or loss when you sell a security. For Restricted Stock Units (RSUs), the IRS considers your cost basis to be the fair market value (FMV) of the shares on the date they vest.

Here’s what that means in practice:

- When RSUs vest, the shares are taxable as W-2 income (subject to payroll & income tax).

- That same FMV becomes your cost basis for future capital gains purposes.

Example:

You receive 1,000 RSUs. On your vesting date, the company’s stock is trading at $25.

- $25,000 is added to your W-2 as income.

- Your cost basis per share is $25.

When You Sell: Capital Gains or Additional Income?

What happens when you sell the vested shares depends on how long you’ve held them:

Holding Period | Tax Treatment | Rate |

<1 year | Short-Term Capital Gains | Taxed at ordinary income rates |

>1 year | Long-Term Capital Gains | 15–23.8% for most high earners |

Selling shares right after they vest? There is typically a nominal capital gain or loss associated with the transaction.

Holding for growth? You may benefit from long-term capital gains, but now you’re exposed to market risk.

Mistakes That Cost You: What To Watch Out For With RSUs

Ignoring Withholding Gaps

Employers often withhold federal taxes at a flat 22% rate on RSU vesting events.

For high earners, this may fall well short of your true marginal tax rate (which could be much higher than 22%).

Planning Tip: Review your year-to-date tax withholding and set aside reserves or increase estimated payments proactively.

Overlooking Brokerage Form 1099 Inconsistencies

When it’s time to file taxes, Form 1099-B from your brokerage may not reflect your true cost basis. Many 1099’s report:

- Zero cost basis, or

- Incorrect basis, especially if shares were withheld for taxes.

This can result in double taxation unless you manually adjust the cost basis to match the FMV reported on your W-2.

Tax Planning Strategies for RSU Recipients

Sell Immediately to Minimize Risk and Simplify Taxes

Once RSUs vest, you’ve already paid taxes. Selling the shares right away:

- Avoids the risk of unintentionally building a concentrated position in your employer’s stock.

- Creates liquidity with no additional tax consequences (if FMV = sale price).

This is a practical approach for:

- Paying down high-interest debt

- Building emergency savings

- Covering upcoming tax bills

Diversify Concentrated Positions

Holding a lot of company stock? Then you’re exposed to single-stock risk. Especially problematic when your income, bonuses, and benefits also come from that employer.

Using RSU proceeds to build a more diversified investment portfolio helps manage downside risk and long-term volatility.

Donate Appreciated Shares for Maximum Tax Efficiency

Held RSUs that have gained value post-vesting? Consider donating shares directly to a donor-advised fund (DAF) or qualified charity:

- You avoid capital gains tax

- You receive a full value charitable deduction (assuming a 12+ month holding period)

This can be an effective way to offset high-income years while satisfying charitable intent.

Use RSUs to Fund Roth Accounts

Selling vested RSUs and using the after-tax proceeds to fund Mega backdoor Roth contributions can help shift assets into a tax-free growth account.

Financial Planning Opportunities

Many RSU recipients fall into the trap of reacting to vesting events. With the right planning, RSUs can serve as a strategic lever in your broader financial plan.

Here are a few common use cases:

- Pre-fund 529 plans or custodial accounts for children using vested RSU proceeds.

- Pair RSU sales with charitable donations to offset income.

- Consider it fun money and go make guilt-free memories. It’ll be the best money you ever spent.

If you want a thought partner to help manage your RSUs, especially when it comes build a cohesive strategy regarding how to unwind multiple forms of equity comp (Options, ESPP, RSUs, etc), we should talk.

If you have questions or would like to learn more, please schedule time with me here so we can have a personalized conversation.

Want to receive exclusive insights delivered to your inbox every other Saturday? Sign up for RLN Wealth’s newsletter.

Ryan Nelson, CPA, CFP® is a Wealth Advisor based in the Minneapolis–St. Paul area, serving corporate professionals with equity compensation virtually across the United States and locally throughout the western suburbs of Minneapolis, including Wayzata, Minnetonka, Plymouth, Maple Grove, Chanhassen, Victoria, Excelsior, and Medina. Outside of work, Ryan enjoys traveling with loved ones, hosting family and friends at his lake home in Northwest Wisconsin, running, discovering great Italian food, and enjoying an americano from an independent coffee shop.

This material is intended for informational/educational purposes only and should not be construed as investment, tax, or legal advice, a solicitation, or a recommendation to buy or sell any security or investment product. Hypothetical examples contained herein are for illustrative purposes only and do not reflect, nor attempt to predict, actual results of any investment. The information contained herein is taken from sources believed to be reliable, however accuracy or completeness cannot be guaranteed. Please contact your financial, tax, and legal professionals for more information specific to your situation. Investments are subject to risk, including the loss of principal. Because investment return and principal value fluctuate, shares may be worth more or less than their original value. Some investments are not suitable for all investors, and there is no guarantee that any investing goal will be met. Past performance is no guarantee of future results. Talk to your financial advisor before making any investing decisions.