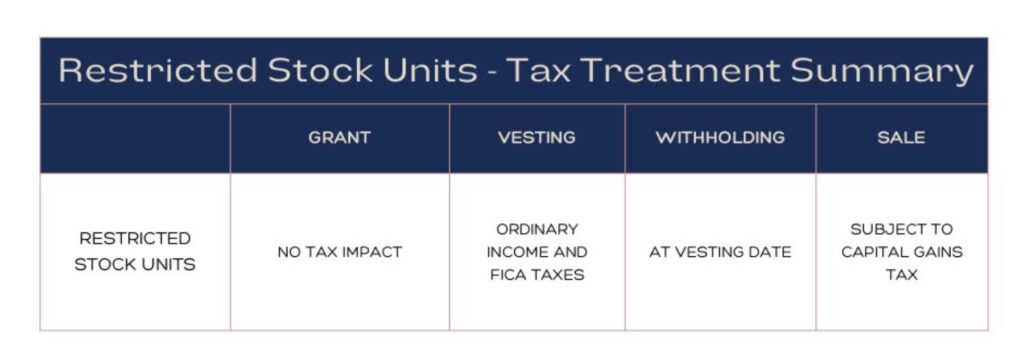

- They are taxed as ordinary income at vesting. When the risk of forfeiture (AKA when the shares ‘vest’ and are transferred to you) is removed the FMV of the shares will be reported as ordinary income in the tax year the shares vest. Note > The price on the grant date is irrelevant.

- Taxes (Federal, State & FICA (Payroll Taxes)) are withheld at vesting. Federal and State supplemental wage withholding rates will apply to your RSU income. Typically, this will be 22% at the Federal level (which is probably not enough withholding) and will vary by state (Minnesota, for example, has a supplement withholding rate of 6.25% – which is also likely not enough withholding!). Note > Amounts in excess of $1M will have Federal withholding of 37%.

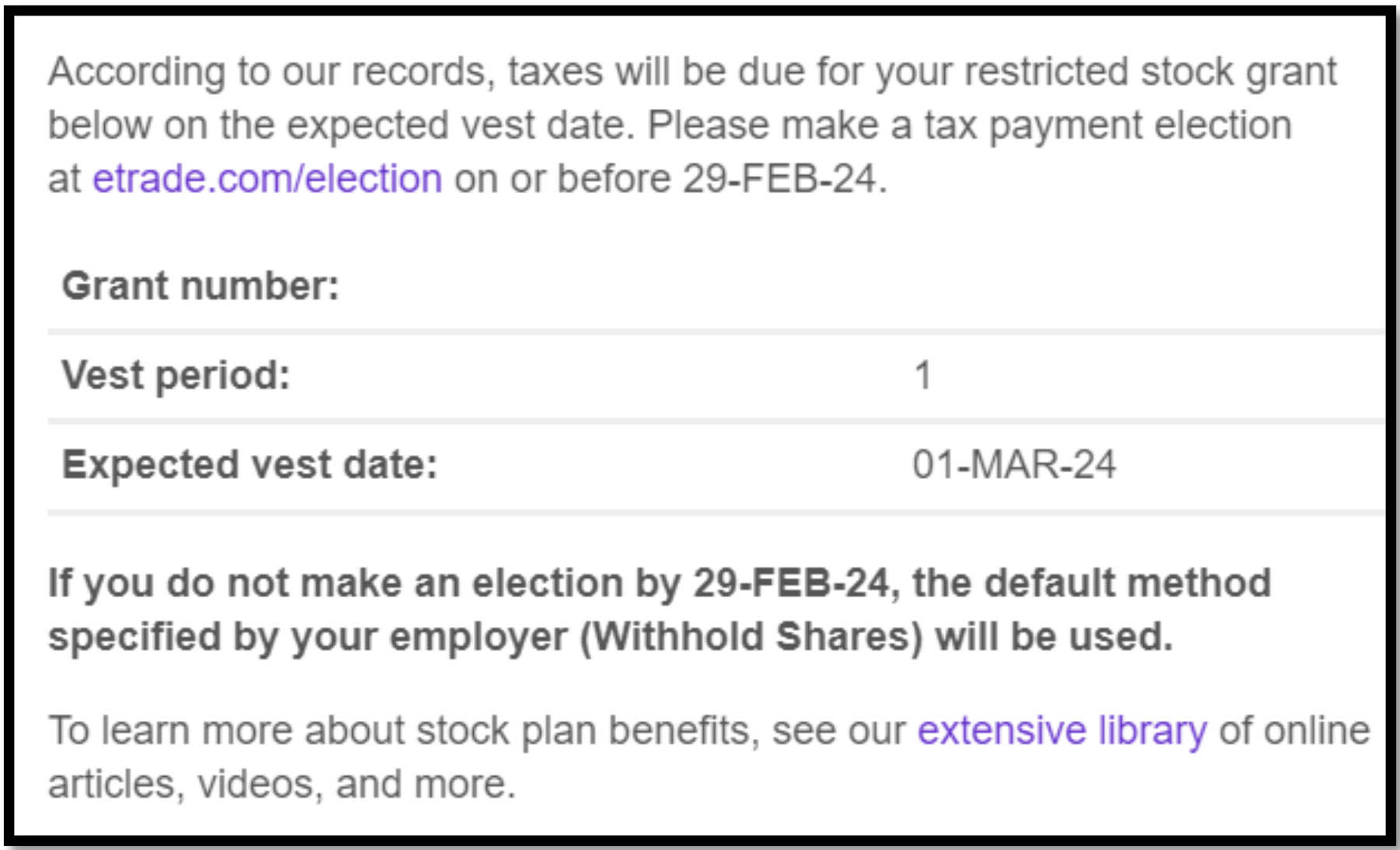

- Ensure proper withholding elections. You will need to make tax payment elections at your custodian prior to the vesting date. Typically, you have two options.

1) Withholding shares (sometimes mandatory) – This is when a portion of your equity award is withheld for taxes and the net share amount is transferred to your brokerage account.

2) Cash Deposit – You may have the option to deposit cash into a brokerage account to cover the necessary tax withholding.

You will typically get an email reminder from your custodian to make withholding elections. Don’t miss it!

- Income recognition from RSUs may trigger other taxes –

a. NIIT (Net Investment Income Tax) – Taxable income from restricted stock units could push your income above the NIIT threshold, causing your other investment income to be subject to an additional 3.8% tax.

b. Additional Medicare Tax (0.9%) – If your total wages are in excess of $250k (MFJ) / $200k (Ind) your RSU income will also be subject to a 0.9% additional Medicare Tax. - Tax Reporting – Fair Market Value (FMV) at the date of vesting is included in W2 compensation. Note > Eventual sale will be reported on 1099-B and the tax basis (the amount you already paid tax on) needs to be reviewed for accuracy to avoid tax overpayment.

- Capital Gains – If shares are held post-vest, then any increase/decrease in the FMV of the shares will trigger capital gains/losses upon the sale of company stock. The holding period begins when the shares are delivered.

- Recipients of RSUs lack control of taxable event – Unfortunately, individuals that receive Restricted Stock Units cannot control when they must recognize taxable income. This is all predefined in the award grant notice. However, you should still proactively plan to evaluate future tax liabilities and determine if holding the vested stock makes sense for your financial plan.

- Dividend Equivalents – Although not required, some plans may allow for dividend equivalents to accrue up to the vesting date. When this happens, those dividends are typically paid in shares.

- No need to worry about the Alternative Minimum Tax (AMT)! – Unlike Incentive Stock Options (ISOs), RSUs do not create phantom income via the Alternative Minimum Tax.

- Beware of double trigger – Pre-IPO companies have a tendency to structure RSU grants so there are multiple vesting provisions. One is usually time-based, and another is tied to a liquidity event. Without both, vesting doesn’t occur.