Contrary to popular opinion, there are several things you can do to improve your investment portfolio in a down market.

Are these wholesale changes or material strategy modifications? Usually not.

But if you start stacking a few of the opportunities listed below during a market selloff, your future self will certainly be happy with your prudent decision making during uncertain times.

Sell / Donate Individual Stocks

Here’s your chance.

Those random individual stocks you’ve accumulated over the years can now be sold at a fraction of the tax costs (or perhaps at a loss!).

Sure, it’s challenging to let go of what you thought was a great decision, but now is the time to take a really hard look at –

- What you own

- Why you own it

- How it fits into your portfolio

- And how it has performed relative to a simple basket of index funds.

And before you go beat yourself up over a bad decision, it’s worth noting that the greatest investors of all time do one thing really well.

They bury their pride and cut their losses (even if it means recognizing reasonable capital gains) with underperforming investments.

“Letting losses/underperforming assets run is the most serious mistake made by most investors.” – William O’Neil

Additionally, if taking gains to clean up your portfolio doesn’t sit well with you, you can donate the individual securities.

Assuming the securities are LTCG (long-term capital gain) property, you’ll get a tax-deduction for the full fair market value of the positions donated.

It’s a much more tax efficient way to satisfy charitable giving goals.

Deploy Excess Cash Reserves

“I’m going to wait for the dust to settle.”

That’d be a great strategy if the market gave the ‘all clear’ signal, but unfortunately it doesn’t work that way.

By the time you realize what’s happened, the market will have already ripped 10-20% and you’ll be back to where you started – Waiting for a better buying opportunity.

So instead of wasting endless amounts of mental energy trying to time the perfect entry point, perhaps it’s more effective to put a plan in place to deploy excess cash reserves in a rules based, systematic way.

But what exactly does that look like?

Here’s a simple approach to getting your excess cash invested –

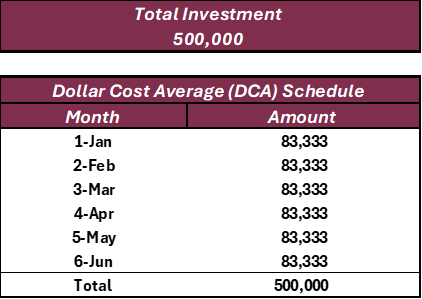

- DCA (Dollar Cost Averaging) – This is a fancy name for spreading out your investment of cash across a number of months (typically 3-12). It takes the guesswork out of trying to buy at the perfect time, and instead provides a premeditated script for when, and how much you will invest over a defined period of time.

Here’s a quick example –

Adoption of the DCA methodology requires acknowledgment that more sophisticated models to deploy cash into the market are inferior and much more time consuming to execute.

Note > Returns are typically greater if one simply invests all of their available cash into the market on one day. You can read more on this here.

An alternative technique is a DCA strategy with a Market Trigger – This approach layers a ‘market trigger’ on top of a DCA schedule. The market trigger, for example, a 3% drop in the S&P 500, would accelerate the next tranche of the DCA.

Here’s a simple example based in the DCA schedule above.

On January 1st $83.3k is invested across a predetermined set of index funds.

The next scheduled investment of $83.3k would take place on February 1st, however on January 17th the market drops 3%.

The market trigger would accelerate the February investment, and $83.3k would be invested on January 17th instead of February 1st.

If the S&P were to fall another 3%, then the March investment would be pulled forward as well.

This strategy puts an opportunistic spin on temporary turbulence in the markets and would continue until the entire investment is deployed.

Transition from Mutual Funds to ETFs

Mutual Funds and ETFs are two different investment vehicles that can offer broad diversification in an investment portfolio.

While utilizing either can be an effective diversification strategy, ETFs are far and away a better option for tax efficiency. Here’s why.

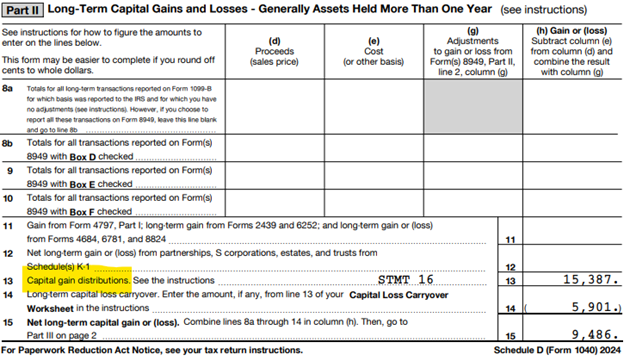

Mutual funds can kick out capital gain distributions. ETFs don’t.

These are distributions at the fund level that require income tax recognition, even though the mutual fund owner didn’t sell shares of the fund throughout the tax year!

Said another way, you have absolutely no control over when this income hits your tax return unless you sell the fund.

Here’s what it looks like on a tax return –

If you have a material figure on line 13 of Schedule D, it warrants further investigation by diving into the details of your 1099.

A consolidated 1099 typically has an itemized list of all the funds that had capital gain distributions during the tax year.

From there, you can assess whether viable ETF alternatives exist for any or all capital gain distribution funds, while also evaluating total transaction costs—including tax implications, transaction fees, and potential fund management fee savings.

Roth Opportunities

- Roth Conversions – In the right tax situation, Roth conversions can make a lot of sense to execute in down markets. You get the benefit of converting assets at compressed prices, and once markets stabilize, your conversion investment growth is tax-free.

- Increasing Roth Contributions – Perhaps a more palatable approach for high income households, simply changing the mix of 401k contributions from pre-tax to Roth can have an equally as beneficial outcome as executing a Roth conversion. You’re giving up the benefit of the immediate tax benefit of pre-tax deductions, but select situations may warrant temporary adoption of this strategy to ensure proper allocation across tax buckets within an investment portfolio (tax-deferred, tax-free, and taxable).

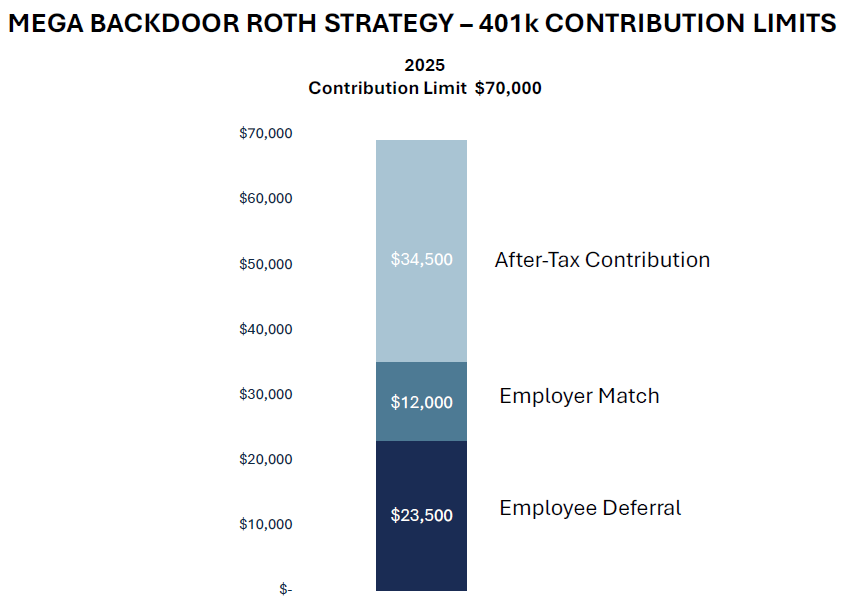

- Mega backdoor Roth – Those with a super saver mindset should take a hard look at the mega backdoor Roth opportunity, if your 401k plan allows it. This strategy keeps the immediate benefit of maximizing pre-tax deductions to a 401k, but allows for incremental contributions to a 401k plan that are considered ‘after-tax’ contributions.

This means the maximum contribution in the 2025 tax year is as follows (with a hypothetical employer match) –

It’s not uncommon for households to struggle to save the maximum every year, so intentionally executing the strategy during down market years can be an opportunistic strategy for those wanting to slam as much cash as possible into Roth accounts.

Exercise Options

There’s a strong argument to be made for exercising stock options during down markets. Here’s a few reasons why –

- Lower Taxes – When you exercise NSOs (Nonqualified Stock Options), you’re taxed on the difference between the stock’s price and your exercise price. If the stock price is down, this spread is smaller, reducing your tax bill.

- Start Capital Gains Clock – Holding shares for over a year after exercising can qualify for lower long-term capital gains tax rates. Exercising now starts that clock earlier.

- Reduce AMT on ISOs – For incentive stock options (ISOs), a lower stock price reduces the AMT impact, making it easier to exercise without a big tax hit.

- Upside Potential – Exercising at a lower price lets you own shares at a discount, positioning you for gains if the stock rebounds.

Tax Loss Harvesting

The optimal outcome of tax loss harvesting is to lock in temporary losses permanently for tax purposes, while maintaining similar (but not identical) market exposure.

To do this, it’s important to have a vetted list of substitute securities ready for bear markets.

Once you have that list, it’s as simple as selling the security with unrealized losses and subsequently buying a substitute security with the sale proceeds.

Then, after a short period of time, you can repurchase the original security.

Planning note > Make sure your substitute securities are not identical, or substantially similar. If they are, your losses will be suspended (but not lost) due to wash sale rules. You can find more on wash sale rules here.

If you have questions or would like to learn more, please schedule time with me here so we can have a personalized conversation.

Want to receive exclusive insights delivered to your inbox every other Saturday? Sign up for RLN Wealth’s newsletter.

Ryan Nelson, CPA, CFP® is a Wealth Advisor based out of Minneapolis / St. Paul and serves clients virtually across the United States. Outside of work Ryan enjoys collecting memories by traveling to tropical locations with loved ones, hosting family and friends at his lake home in Northwest Wisconsin, running, searching for great Italian food, and enjoying an americano from an independent coffee shop.

This material is intended for informational/educational purposes only and should not be construed as investment, tax, or legal advice, a solicitation, or a recommendation to buy or sell any security or investment product. Hypothetical examples contained herein are for illustrative purposes only and do not reflect, nor attempt to predict, actual results of any investment. The information contained herein is taken from sources believed to be reliable, however accuracy or completeness cannot be guaranteed. Please contact your financial, tax, and legal professionals for more information specific to your situation. Investments are subject to risk, including the loss of principal. Because investment return and principal value fluctuate, shares may be worth more or less than their original value. Some investments are not suitable for all investors, and there is no guarantee that any investing goal will be met. Past performance is no guarantee of future results. Talk to your financial advisor before making any investing decisions.